For the income portion: I’ve been doing equal parts HS3EZ, 488 and 484 along with an ATM campaign leaning bearish. This helps provide a lot of diversification.

For the convexity portion: I’ve been doing BSH factory + opportunistic entries of additional black swan insurance (haven’t had to since Feb).

I’ve just started using a base LTI as well

Pretty boring, pretty simple. I’ve found now that I rarely care or even look at what the market is doing. I just enter and add adjustments when required. The first quarter was great and so far April is pretty stagnant but with a lot of potential and I’ve got a solid formed campaign both for the income and convexity portions as well as live LTI. Looking good into finishing Q2. That 48x theta has to come in sometime.

That’s pretty much the summation of how I’ve been running trades through the year. Very boring weekly entries of 48x and HS3EZ plus the management of the convex black swan portfolio. Systematic with intent and with little regard to timing of markets re entries and adjustments. It works.

The intent is to continue to investigate variants and other trades that provide some diversification to the portfolio but I haven’t had anything really pop out. I’ve got some interest in the 0DTE and looking at it from a professional gambling standpoint re edges and trade sizing but I just haven’t had the ability to jump in yet. Probably a summer thing. I will probably finish up a 486 backtest to add to the research. That’s probably all that’s on my radar.

I can’t go into the individual trade compositions because of community privacy etc but you can get more information at the mastermind group, Ron Bertino runs a few awesome well constructed courses there and the community you can become part of is a private one where we share info and strategies and as such we’re mandated to keep specific details private as it’s not fair to others in the group.

Didn’t get as much as I wanted done because …Holidays and distractions… enough said 🙂 Despite that, I’ve hit the ground running and I am working on creating some meta portfolio management which I mentioned in my last post. The idea is to really take advantage of diversification across strategies that aren’t correlated to create a combined time series that provides increased geometric returns by way of lower drawdowns and better compounding. What Mark Spitznagel coined as a volatility tax. We reduce that and pay less “tax”. If you have a lower return each month but you have less draw down, you compound it better than a higher more volatile strategy and so on. To me, it’s all you can do, diversify (smartly) and not just for the sake of diversification but true meaningful diversification. I wouldn’t ever just put all my eggs in one single strategy in one single week with a planned capital the size of my portfolio. There’s just too much reliance on how those specific strikes and BSH will react. Plus, it’s sorta fun having previous entries mature and act as mid bear hedges, harvesting and knowing that a single entry with bad timing is only 1/10th (well really 1/30th) the portfolio is a nice thing. It takes time to build up sure but it’s like 2.5 months. Who cares.

There’s a series of OTM (out of the money) type strategies (3 of them that I use) combined with a bearish toned ATM (at the money) trade to pick up the middle bear (non crashy moves ie Aug 2019, Oct 2018, Dec 2018, Jan 2016). Each of the OTM income portion is diversified in mostly its strikes but also the type of BSH it uses to pick up during a crash. A 488 will react differently then a 484+BSH then a HS3EZ (not saying I use those well, maybe idiosyncratic versions of one or more of those) both in it’s income production and income engine as well as its black swan hedge that it utilises. There’s some diversification, it’s not perfect but we work to reduce that imperfection by time diversification across 10 week campaigns (1/10th at a time) along with 3 additional BSH/Vol hedge type campaigns. The 3 BSH vol hedge type campaigns are factory based (ie they build up over time) and they are meant as a triple redundancy insurance towards the 4 other income strategies. But in reality, they should produce lotto like returns in a crash. One of the BSH/Vol type hedges actually generates income and helps compensate the costs of the other two. We then have as much redundancy as we possibly can both in the income strategies by way of time, strike/skew diversification, and BSH diversification built within the income strategy plus we have 3 additional BSH like stand-alone factory type strategies that should provide full assurance during a a crash and most likely a lotto return. Not sure you can do much more than that.

It’s systematic and the fact that you’ve got 10 different things to manage reduce human factors at a cost of management complexity which is my job anyways.

Speaking of which, I feel lucky to have found something that I wake up looking forward to and what will likely occupy the rest of my working life. I doubt in my life that I’ll ever pursue entrepreneurial projects again. I went through my 20s and 30s setting up some successful businesses w/ my wife and two other partners that I still manage (mostly as a board member). I give over-arching direction and make sure things are running in line with the plans set forth but there’s no day-to-day which set me free. We started the business in 2004 and I finally got out of the day-to-day around 2017. I just never liked dealing with humans and human issues in the workplace. It gets complex quickly and is often irrational and I feel just out of control when dealing with human resources. I know that’s super odd to say but maybe I can expand on it. I started a software company and I am not a software developer. Maybe that helps 🙂 I have to rely on my team to correctly advise me while making business decisions and dealing with customers demands while having an expertise that was relevant but outside the central operation of the business. Make decisions, go back to team, they tell you impossible, you know it is possible but can’t be quite sure because your experts are advising you and you fight and they end up getting it done /// rinse repeat. I always wanted my “money making” life to be me and a screen and that’s it. Very few outside “human” variables, very little reliance on anything but myself, my decision and the game environment we call the market. When something went wrong, it was something that was on me. Something that I could perhaps think my way out of. Not something where I had to rely on someone else. That was my goal and though it took like 5 years to really work that out (trading is hard…mostly because you have to meet parts of yourself that you might be unfamiliar with…and protecting yourself from yourself takes practice and time..and really just a system and recognition).

In my opinion, the attributes (besides the obvious skills) necessary for successfully trading is self reflection/humility, ability to take risks and tenacity. If you lack one of those, it ain’t going to happen. The risk taking portion has to be smart, unemotional and well thought out..with outs and with a system. One thing I’ve learned in life and I’ve seen it time and time again is that you can’t talk many people out of taking risks when they’ve become emotional about it. I can list like 10 situations which made me cringe and are very poignant lessons, some are horrible. It’s a specific type of person too. If someone decides that they are going to gamble, take a business risk, buy a stock, or whatever it is that has a possibility of changing their life trajectory, I found that it’s often very hard to talk someone out of that risk even if you give them good reasons. .Once they make an emotional decision, that’s it. But, if someone is humble and self reflective you can often advise them against and they back off and reflect. If you do take that risk, you need outs and you need to become tenacious (that’s where tenacity comes in). I took loads of risks in my 20s that I should never have, and now I have a process that protects me from making emotional decisions…I did have that tenacity though and the risks weren’t emotional though they were probably way to high a risk of ruin. Unfortunately, for success, you often really need the ability to take risk, you just can’t do it with emotional baggage. When I took those risks, I’d be like fuck ok…I’m in it now, then I’d create outs and I would literally not stop (sacrifice sleep (80 hr weeks) to make these risks work out. Stupid but tenacity got me out of jams and I learned that we often take risks for excitement, for that dopamine rush and to be very mindful of that. This is why you often can’t talk someone out of an emotional risk, they have already decided they need this rush this thing that can change their life (or destroy it) because they need to feel. When you do take a big risk, make sure you have control, several “outs” and be ready to commit your entire being to making sure you don’t fail. Tenacity, Risk-taking and Humility are the key ingredients. Look at the logo on my plane tail. Badger (Tenacious little fucks).

On to personal stuff, I got up in the air twice so far since being back (quarantine affected that). What a wild experience though, we flew to Muskoka (took 24 min from Brampton), then over to Toronto to do a fly over of the city. We asked the tower to do a direct fly over of YYZ (the busiest airspace in Canada) and was approved. This is a once in a lifetime thing to do…it was EERIE cool. Not a single flight (landing or take-off) and completely empty. Here’s some pics. I’d write a whole lot more on the blog re what it’s like to do a PPL in a Cirrus SR22 if anyone had interest. I just don’t want to bore.

Back in the plane. No better place!Downtown core (CN Tower and Sky Dome) Direct fly overYYZ EMPTY! Busiest airspace in Canada. Pandemic effects..My Baby. 3-4-5 Papa Kilo.

Made my way to our new temporary home for the winter and spring. The place will be our forever home in Canada and act as our main base. We still are trying to figure out if we’re going to make our way to LA for the kids education but we’re getting tired after this last build and move so who knows. That said, I miss how easy things were in Cayman, it was like a free-for-all in terms of pretty much anything/everything re being able to just live life. I am met with blocks on everything here in Canada. Everyone seems to want to create problems. It’s bizarre. They won’t even accept my international license or cayman license and want me to start off with a learners permit, they’re having a fucking laugh. I’ll just continue to use my Cayman license, just means I can’t register my cars until I can find some Canadian insurance company that would insure me without a CAD license. I also find myself talking on the phone to customer support for hours a day for a variety of things as well. Real life sucks apparently lol.

We’re here until at least the summer and though we’re 90% going to LA, there’s a small chance we’ll fall in love with this property and stay here. Though, man, I just don’t know if I can “regular” life it here like I said above. It’s probably irrational but there’s a lot of weird feelings about raising the kids here and I mean, its fucking’ cold. Though, having the plane now gives me some pretty cool options to escape and the hangar is literally 12 min from my house. I can fly to Myrtle beach in like 3.2 hours for instance. The property is 100 acres located just 25 min from Toronto international. So the location is perfect and close to the international airport and acts as a great base to our families (we’re both from area originally and our families are here). That was the intent…have a second home near our families but it became much much more than that as the project developed and the budget increased…..

One of my best friends designed and built it same as he did for Cayman so it’s been a fun challenging project and his tenacity for efficiency, his skills and his ability to keep the project a value creation device has allowed for a valuation much higher than what was put in. So I am super happy and both projects have provided me with value. He’s been actively helping me manage investments so it might be his pièce de ré·sis·tance or swan song as he moves more towards trading. Or perhaps he continues on but treats it like a hobby or it’s a bit of both. Who knows. Here’s a few cool pictures of the property (which isn’t 100% complete yet but liveable). It’s got a VR/Sim room which will be decked out with a star wall, RGB lights, and 4 setups (our family are PC gamers…no XBOX whatever or PS whatever allowed in here!). We have a sweet swimmable hot-tub on the second deck, an infra-red sauna, several cool fireplaces, a speak-easy etc. It turned into a true chalet like experience. Our furniture hasn’t yet arrived but I think it’ll be here in 1.5 weeks. We’re making due with what we have, it’s exciting because so much is not done and we’ve got limited furniture so it’ll only get better. Fun and frustrating at the same time I guess.

Probably the only space that’s 95% completed. The entry.The outdoor ceiling is not complete yet but it’s coming!Void of furniture but what a view!It’s coming…Missing the furniture but it works!

We landed in CNC3 a few weeks ago and hangared the plane. I still need some more hours but the weather has been shit and instructor availability as well. Things happened slower then I hoped. I really wanted to come back licensed fully.

The entire break I’ve been concentrating on meta portfolio construction as a means to reduce drawdown and increase geometric returns. I’ve come up with using 3-4 OTM style trades that we talk about in the PMTT Group as a base income producer and with my own spins and each are composed of 4 different types of BSH. These are put on in campaign style with the average being about 10 weeks of campaign. This gives time diversification. So we’re now diversified in entry timing, OTM income production and BSH provision. On top of this, I combine 2 black swan type campaigns that provide additional protection over all. Then I have an aggressive harvesting style that really translates into back ratios at a variety of strikes on older maturing trades. So basically, 10 different time entries, 4 different strategies, 4 different BSH styles, a bonus 2 hedge type factories and harvesting. About as tight as you can get.

4 Types of Out-of-the-money income strategies put on across 10 weeks giving time, strike(skew) diversification

4 Types of BSH protection put on across 10 weeks giving time, strike (skew) diversification

2 bonus types of BSH factories/hedges put on in campaign style across 4-6 weeks giving skew and time diversification and 2 additional fail safe swan protections

Harvesting aggressively all structures that are matured

You’re left with creating less draw down and increasing compounding returns which is equally important to the trade strategy itself. It add complexity sure, but I mean, this is all I really do now and it’s systematic. That’s a preferred method for me.

I’m finalising all the time series for each of the campaigns from 2014+ and I’ve noted that there is adequate response differences to a variety of environments and together they provide a smoothing of return. In my mind and as I mature as a trader and as I have started getting consistent results, I’m convinced that the key to success at trading for a living comes with diversification both in time and in strategy. You take 6 known alpha producers and you do 1/6th each. It helps with human factors, as you’re much more likely to follow the system/rules if it’s just some annoying small part of the portfolio not the entire thing. The options market has a funny way of causing you to draw down from the tops.. You’ll be sitting at 80% profit target and one day you’ll draw down to 50% for no reason (market hasn’t moved) and you’re becoming price fixated and often times it does preclude a vol event and from there you’re just waiting for that old 80% to come back because you think you can rely on time. It’s a fools errand not to follow the systems and rules. You’re much more likely to do what you need to do if it’s just a 1/6-1/8th portion of your portfolio.

As mentioned before, the last 6 months have been pretty much straight opportunistic ebb-flow ATM style trades taking advantage of the environment. I’ve just started implementing a systematic portfolio based on the above post and from there that’s all I’ll pretty much do.

I am back at my desk for 8 months so I hope to blog more and post interesting things the best I can.

A nice pop in the p/l given the US is contemplating giving up on those pesky elections. Who needs them 🙂 Delta sitting comfortably at -800 and given the DTE, any moves towards -200 delta and I’ll just start peeling off the trade piece by piece removing risk as I go.

Sep BWBs are currently going for about 95c credit and Oct BWBs are going for about 2.25c. I’ve got loads of flies up in Sep so I can purchase BWBs against those but I didn’t get any in Oct yet so I’d have some exposure to downside if I get some of the Octs on. Not terrible given the deltas I’ve got built up in Sep so I’ll probably put some on today. Usually I like to start with the flies. It’s no different than just entering a rhino/bwb though which loads of people do without the fly hedge/combo.

It’d be a huge milestone to close the Aug at 500k P/L. It’ll call for some real nice champagne. But I won’t fixate on it, I’ll just manage that risk. Huge month so far and I think July is sitting at just over 7% P/L and Aug will likely be similar. Cannot complain and thankful the market keeps on giving.

Had a 30% year last year and I gather I’ll get towards 50-60% this year solely from the opportunities. The last few months, I’ve just been concentrating solely on building that long vol BSH up and trading these Rhino/BWB combos but it rarely takes much more than 30min a day, things are boring when they are producing. Many traders say you’ve made it and are barking up the right tree when you’re trading a system thus eliminating human factors and bias and subsequently the actual act of trading becomes boring. The latter part is true right now, the former isn’t based on a system per say but it will be once this environment ends.

We ended Friday at a delta of -900 after adjustments and now sit around -1700. That shows you just how quickly negative delta you get with time even just the weekend. The position is hovering around 285k P/L so it’s seen an increase of 35k over the weekend. I’ll have to adjust the upside today and by Thursday this will be done with removals from the structure rather than additions to it. There is 25 days to expiration and I’ll aim to remove risks as we go from here until it’s a benign structure that can be expired.

Here’s an update on my big August trade that has about two weeks left in it. It’s starting to actually look like an old school ATM trade given the reduction in VIX and the lack of credits in 30 DTE or earlier trades. From March till June, credits were huge and upside risk NIL. Now as opposed to then, I actually have to use some upside adjustments aggressively.

I started adjusting for upside exposure during this little fall towards 3200. My overall deltas are sitting at -900 and I’ll close out the day at that.

Delta: -939

Theta: 21,956

Vega: -10,567

The position represents 5MM in planned capital and is sitting at 251k profit. I’ll dance this thing into Aug 7/8th and continuously remove risk and adjust. There’s a small chance for an extremely large payoff (the biggest I’ve ever seen) @ 1MM in 1 month. Reminds me of that show 2months 2million. Ridiculous but it is the environment and the opportunities. These types of trades won’t last. For now, I’ll happily let it beef up the account. I’ve got BS protection in case we have some sort of massive gap down.

Here’s the trade looking forward 7 days

Here it is where I expect to close it. It won’t look like this later as I’ll be constantly adjusting back and forth between now and then and the negative deltas will continue to build up as time passes

For a bit there, the VIX hit around 24 and it looked like the ebb and flow trade was about to get a lot harder but today we can now get a Sep BWB for $1.00 credit. So we’re still going for now 🙂 I got some on to offset the Sep position which I started with symmetric flies back at 3260-3270. I’ll be very happy if we can keep getting these conditions for the next 6 months.

In a large fall, and if we approach -400 delta, I’ll start to adjust for the downside and I’ll offset with some way OTM calendars in case of a bounce. I have two trading weeks left for Aug position which will get more and more negative delta and have more and more protection to the downside. If I am forced to adjust for downside next week, it means we went through 3150 area and to offset the nuance of continuously increasing negative deltas, I’ll use some way OTM calendars for upside protection while adjusting for the asymmetric risks on the downside.

I gotta say, I feel kinda lucky that I was also able to start the September position, I wasn’t sure I’d be getting the same opportunities with BWB pricing. Perhaps this continues on for the rest of the year re elections in Nov. Eventually I will move on to a 488 campaign, BSH factory, TAA and ATM at lower PC.

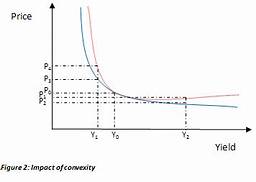

Given the events of February/March 2020, I had to re-evaluate risk and its presentation in each of the components of my portfolio. Though it was beneficial to add what I consider a god level data point for backtesting purposes, it was not fun to go through. It was the fastest decline and recovery in history. There is no tougher environment to trade through with complex non-directional options strategies. I ended up positive through the event despite the fact that things were broken in the market structure. Things happened that should not have happened. I saw things that I am sure I’ll never see again. This allows me to reconsider risk through what was one of the most market destabilizing events in history. This breaking of various markets and market components has given me a peek into what was naked when the tide left and allowed me to dig deep into my compositions and fine tune with risk management as the main motive. It motivated me to create a systematic approach to my base trades for entries, exits and adjustments. It took 4 months of hard work, but I’ve designed a system that accomplishes all of the risk management goals while maintaining returns that will compound better than before due to the reduced drawdowns. The key to this is maintaining global convexity despite being locally concave in risk profile. This means that risk where it is defined and quantifiable (local risk) while maintaining/financing the ownership of global convex risk on the tails. Short locally and long globally.

The more variant a portfolio is the more it impacts your geometric return. I have an edge, but if I am in extended drawdown, there’s less capital exposed to that edge. The less you draw down the higher your geometric return. It’s the power of compounding and is what Mark Spitznagel calls the volatility tax. The big losses are all that matters to your rate of compounding. Makes sense right? Manage your risks, maintain an edge and let compounding do its magic.

My primary interest lies in the long volatility tail space and coupling that with localized complex option income production. Globally convex locally concave. The long volatility tail portion of the my portfolio closely corresponds to what Universa, Nasim Taleb and Mark Spitznagel research, it’s a convex payout on extreme market events. When you tie in global convexity (extreme payoffs in extreme events) think of the convex shape (shown below) with local concavity (necessary for regular income production), you end up with the best of both worlds. Absolute protection and income production on the tails (which are rare) coupled with regular income production locally.

The composition of both elements in the options space has benefits that are astounding as it not only gives you capital during turmoil but it protects both a traditional portfolio as well as one composed of options. You prevent event draw downs and have made significant returns that can be actioned at market bottoms. That effect is exceptional. The combination of long vol with a traditional income strategy is what allows for the highest geometric return profiles.

Coupled with the long vol tail hedge, I’ve worked on systematizing the income strategies that are completely mechanical in nature. There is no room for human bias. I worked out a mechanical system that has no decision bias in both the long vol component as well as the income production component. It prevents the human factors issues that can cause mistakes and under performance.

We’ve got so many great data sets now, we’ve got the vol events of Aug 2019, the bear shocks of Oct and Dec 2018, the volmageddon of 2018, the time skew issues of Aug 2017, Aug 2015, Jan 2016 and so on. We’ve got a plethora of data. The period from February to June of 2020 used this data to do a deep dive into restructuring the portfolio and analyzing its risk factors. It was long, arduous and sometimes frustrating when you realize that everything has risk and the only true way to eliminate or minimize is by true diversification.

The lock down forced me to work long hours daily to re-evaluate my systems and to fine tune a new system setup. This was a period of heavy backtesting, reading, daily hour long phone call discussions with a trade buddy, trials, and analytics. I left no stone unturned even exploring things I would normally say was trade style heresy. The main discovery is the need for systematized approach in all base core strategies. The management is systematically rules based. My entire portfolio will follow this tenant. It’s a minimization of human factors. As Jerry Parker puts it :

“We are not really interested in people who are experts at the french stock market or german bond markets due to technical nature of trading…it does not take a huge monster infrastructure: neither Harvard MBAs nor people from Goldman Sachs…I would hate if it the success of Chesapeake was based on my being some great genius. It’s the system that wins., Fundamental economics are nice but useless in trading. True Fundamentals are always unknown. Our system allows for no intellectual capability.” Jerry Parker

Related to the above statement, I’ve had a realization to systematically use quantitative analysis and trend indicators to manage trades with respect to risk, entries and exits. QA gives me a way to manage the trade risks systematically while keeping me on the right side of the market trend, it’s what the university endowments use and it’s what Jerry Parker helped systematize in the 80s and 90s. I am using it to err the trades in the direction where the sum of the quantitative analysis points us. The delta adjustment range is -3 to +3 per unit. If it’s a bearish trend, we’ll keep it in the -3 range and if it’s a bullish trend we’ll keep it in the +3 range. Lastly, it lets us know when to exit trades. If we use Vix/Vix3M ratios, force index, OBV, ATR expansion etc we can avoid every major event in the last 10 years. I have now incorporated mandatory exit signals. If the signals do not show and we have a black swan, that is protected as well because of our long vol component.

It’s important to have a system that removes emotions and biased decisions. It removes human factors and that gives you something that’s concrete and sustainable. Decisions cause fatigue especially when tied to large money. Through the lock down, I tried investigating several things with an open mind, including taking advantage of zero day premium trades (PR hedgies) and cycle indications trades. This led me to making polarized decisions on an hourly basis. That’s not sustainable, it’ll exhaust and it’ll burn out. It solidified my requirement for a systematic rules based core portfolio. You can adjust/fine tune the rules but you cannot disobey them once they are live.

On the 8th of Oct, the market fell pretty hard into close and the skew/vol were favourable to enter a 488 STT, so I did. I allocated about 25% of the planned capital as the conditions weren’t quite good enough for a 50% or full entry. I was able to cash out at 40% profit target the next day. I did. Why did I only do 25%? There’s probably 25 entries since 2014 where I’d go 100%, however that said, I have to re-evaluate my criteria as it was implemented for the 484 which is a slightly different trade. I may lessen the requirements for the 488 by a fear spike and VIX 18+ for at least a 25% allocation. (VIX is really a very crude way to measure the entries, I just say it because everyone knows it and what it represents re market conditions..but in reality I’d be looking at a whole slew of things to determine entries). If VIX is above 27 and we have a capitulation day, I’d probably switch to 484s unprotected but everything below that I think a 488 might be the answer. I still have to confirm backtest everything and how the exact opportunistic entry system will work but for now it’s a start.

As mentioned a few times, right now my portfolio consists of a blend of a TAA base, some bond rotation (low vol–municipalities, senior loans etc etc), a strategic LTI portfolio, some sectors rotation and a cute factors system. The above represent a 0.75:1 on capital. Then on top of that, I have an active BSH factory for income and lotto. The BSH factory method I use now produces 18-20% a year but will return incredibly during an Aug 2015 (161%) or Feb 2018 event (62%). This is a producer in large events (crashes). On top of that I have 15% allocation to at-the-money (ATM) options trades such as the Rhino and bearish butterfly. If we have any large vol events (opportunity) I’ll enter 488s and 484s. This is my portfolio.

I closed out most remaining options trades except the allocation I have to ATM Rhinos. I have a bit of January left and that’s it. I will work to close those as the next week or two go by. Mostly in cash in terms of options allocations. I am forming a new BSH factory to try and up it’s size relative to my account, it was a bit lower. Not a whole lot else to report on re trades.

The account just hit 30% for the year which puts me at about 10% a quarter. Happy about that. I was hoping for a better (greedy) end to the trades but the market movements prevented that. The market stayed in the upper range and started to tap on 3020 which forced me to start balancing the upside risks and after about 10 days I just decided to lock in profit and remove significant portions of the trade. If I had done nothing, this sharp little 160 point drop would have netted much more. Just this afternoon on that very sharp rebound my account hit all time highs so I took half off and removed a lot of my risk. The sharp little flash crash today from 2892 to 2857 had actually knocked the P/L by almost 4% but now its fully recovered and well profitable (and most of the risk is closed).

As mentioned above, I decided to close off half of the account today on the bounce to 2905. The Dec STT dipped down about 60k during todays mini flash crash from 2892 to 2855, albeit that’s likely just temporary due to option pricing gaps between bid/ask but has since recovered to +10k on the day. Good enough for me and given the market movements and the news climate. I will wait for some opportunistic entries and be happy with the profits to date.

Funny enough, I entered 40 units of 488 yesterday and they hit 1/3rd profit target today on the afternoon ramp. I took it. I’ll always ladder my profits according to days in trade especially if it’s within the first week. One thing we must be careful of is that if these are opportunistic, and you’ve got nothing else planned, then if you start taking lower profits (the profit target is $1k, I took about $380) and you have a max loss of $2k, well, this could be a problem as you’re not capturing enough of the 1k wins to offset the max loss. However, for me, this entry wasn’t the only thing I put on and I mean, it was within one day. Any further down move, I’ll slap some more on with less vol requirements as I had with yesterdays.

I am becoming a big fan of risk reduction via non-correlating strategies. So I am more and more starting to add in a variety of things both as a base as well as opportunistic. I’ve got a solid momentum based TAA along with low vol bond rotation as my base. It draws upon theories from several white paper authors in the tactical asset allocation realm, such as Keller and Keunings white papers on Vigilant Asset Allocation, Protective Asset Allocation, and Generalized Protective Momentum as well as Gary Antonacci’s white papers on Dual Momentum factors and his Risk Premia Harvesting paper. I’ve setup my own little combo of these and other things to create a nice long term strategic base portfolio that produces ~11% CAGR on average with a 5% MDD since 1990. Will it produce this in the future? Who knows, but that applies to anything. I worry mostly about the safety rotations ie IEF and TLT and as such I’ve mostly removed TLT as my safety rotation and changed it to IEF (that helps temper expectations a bit) . I mean, the last 10 years, TLT has produced 10% per year which is equity like w/out the equity risk. That won’t last. If we have a long period where rates just stay stagnant the returns are much much less. If rates fall to zero then it’ll be great (initially) but after that any increase will be horrific (for returns on TLT/IEF). So yah, bonds will def underperform going forward and much of these backtests rely on rotation to bonds so we have to be careful not to expect the same, that said we probably have 5 years before we have to worry about this.

I started to add in Rhino’s again and I actually got some on at 86c yesterday. That has to be a record price for me and I’ve been trading them on and off since 2016. That’s another opportunistic entry.

The plan going forward is to run the base portfolio (which consists of 8 different strategies each adding some non-correlation) coupled with the BSH factory, a variety of ATM trades, and finally opportunistic Rhinos and STT.

I recently (and finally) hit profit on that trade I was nursing since Aug 1. I probably over-hedged a bit during Aug as the skew and vol went haywire and the modeled positive deltas were just a bit too overladen with risk. I probably entered 20% too many bearish stt and probably sold a few too many ES shorts but at the time and with the bipolar nature of the market on any tweet, I felt it prudent to eliminate some of the risk. Further, on the subsequent up move I just couldn’t convert the bearish STT as quickly as I’d have liked too but hey profit is profit. There was a lot of whipsaw too that crushed some of my ES short hedges. The big positive was that I managed risk like a boss but the negative is that it’s resulted in under-sized return as I wasn’t able to take advantage of the vol and skew present because I was managing risks of low vol entries. I’m now moving my trades to opportunistic entries only. I’m talking big down days where forced liquidation are occurring.

I’ll end the month of Sep having made about 3% maybe 4% from Aug 1 to Sep 30th. Not terrible given the environment re skew/vol and the news environment. It got a bit crazy there with tweets. I think I’ll end Q3 right at about 30% which is 10% per quarter on average. I am happy with that and it’s in-line with what I figured. The next quarter results will be entirely dependent on opportunistic entries. If we don’t get the right environment, I won’t be able to enter the juicer STT options trades and I’ll be reliant on my base portfolio and BSH factory. Is what it is…happy to wait for opportunities because when they occur it’ll make up for the stagnant times.. The conditions I’d like to enter in have happened just 25 times since 2014 so it’s going to require patience. The returns from those entries are much higher and you can often get out within 11 days (that’s the average length of time). I’ve seen that the trades will produce the same overall, with very small chance of large draw down and very little time at risk. I mean, the average days in trade was 11 and there were 25 of those, that’s 275 days at risk out of 6 years of trades (That’s like 1/7th of the time).

I leave on Friday to Necker to celebrate my 40th and 20th anniversary. I have no idea what to expect, it’s pretty damn ridiculous but we pulled the trigger because well, it’s two huge milestones. Maybe its worth it maybe its not. I won’t know for another 2-3 days. I imagine there’s some life value in going…maybe? Wildy, and good timing, just two days ago I did have a pretty awesome poker score when my coach got 2nd place in a WCOOP and I had a piece of him. It netted me more than enough to cover the trip, and covers poker buy-ins for a while now. LFG. Anyways, it’s a perfect time because luckily my trades are neutered and carry barely any downside risks and I can just unwind and leisurely work on some projects I have going on. The onllly issue right now is that there’s like a hurricane forming and moving right towards where we are going. Hopefully it fucks off.

So I probably have 2 weeks left with my current STTs, I have about 70k theta per week and by Oct 10th I’ll probably be fully out of the market re STT type trades. I’ll have a small BSh factory and some LTI stuff and I’ll be sitting and waiting for a big down move. Any 5-7% move down is while I still have on this structure would be worth a LOT of return (another like 10%)! So it’s welcomed! If that happens, then my luck is disgustingly sick and I’ll be removing the entire thing and entering brand new ones. Easy plans going forward.